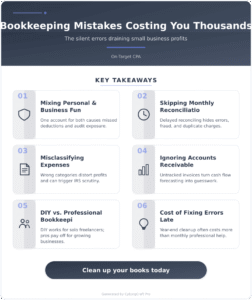

More than half of financial statement frauds involve sales and accounts receivable, according to the Committee of Sponsoring Organizations of the Treadway Commission. (COSO is a joint initiative of five private sector organizations that develops frameworks and guidance on enterprise risk management, internal control and fraud deterrence.) But why do fraudsters tend to target accounts receivable?

For accrual-basis entities, accounts receivable is typically one of the most active accounts in the general ledger. It’s where companies report contract revenue and any other sales that are invoiced to the customer (rather than paid directly in cash). The sheer volume of transactions flowing through this account helps hide a variety of scams. Here are some examples.

Fictitious sales

Sometimes fraudsters book phony sales — and receivables — to make their company’s performance appear rosier than reality. Increased sales assure stakeholders that the company is growing and building market share. They also increase profits artificially, because bogus sales generate no costs. And, overstated receivables inflate the collateral base, allowing the company to secure additional financing.

Timing differences

Unscrupulous owners or employees might manipulate cutoffs to boost sales and receivables in the current accounting period. For example, a salesperson could prematurely report a large contract sale even though material uncertainties exist. A retail chain CFO could hold the accounting period open a few extra days to boost year-end sales. Or a contractor might use aggressive percentage-of-completion estimates to boost revenues.

Lapping

Some employees divert customer payments for their personal use. Then, the fraudster applies a subsequent payment from another customer to the customer whose funds were stolen. The second customer’s account is credited by a third customer’s payment, and so on. Delayed payments continue until the fraudster repays the money, makes an adjusting journal entry or gets caught.

Know the red flags

Accounts receivable fraud can be hard to unearth. Fortunately, experienced forensic accountants know to look for such anomalies as:

• Significant write-offs and returns in subsequent periods.

If something seems awry with your accounts receivable, we can help verify your outstanding balances and find holes in your internal controls system to safeguard against future scams.

© 2016