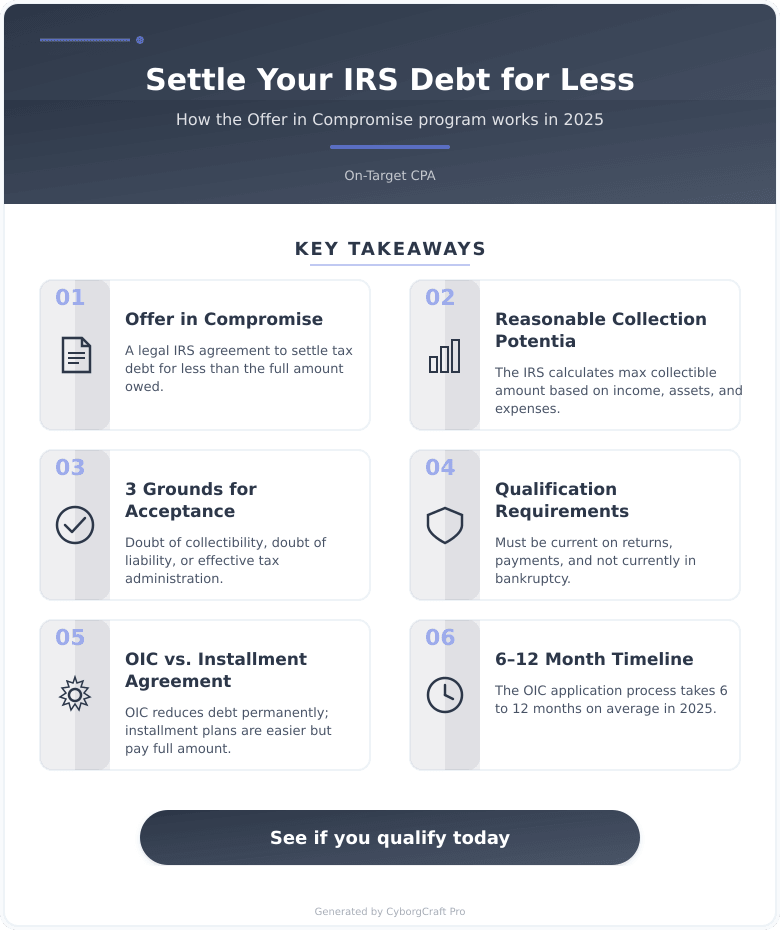

An Offer in Compromise is a formal IRS program that allows qualifying taxpayers to settle their federal tax debt for less than the full amount owed. It exists because the IRS sometimes accepts a reduced payment rather than risk collecting nothing at all.

This guide focuses specifically on how the Offer in Compromise program works in 2025, who qualifies, and what steps to take if you believe you may be eligible.

Offer in Compromise Definition: A legal agreement between a taxpayer and the IRS that resolves a tax liability for less than the full amount due, based on the taxpayer’s ability to pay, income, expenses, and asset equity.

The most common mistake we see is people assuming they automatically qualify just because they owe a large amount. The IRS evaluates specific financial factors, and the process has real teeth. Understanding those factors before you apply can make or break your case.

How the Offer in Compromise Program Actually Works

The IRS bases its decision on something called your Reasonable Collection Potential (RCP) – essentially, what the agency believes it could realistically collect from you. If your offer matches or exceeds that figure, the IRS has grounds to accept it.

Three grounds exist for acceptance:

- Doubt as to Collectibility – you genuinely cannot pay the full debt

- Doubt as to Liability – there is legitimate question about whether the debt is accurate

- Effective Tax Administration – paying in full would cause you severe economic hardship even if you technically could pay

According to the IRS official Offer in Compromise page, the agency accepts a limited number of offers each year, and acceptance rates reflect how rigorously the IRS evaluates each submission. That means preparation matters enormously.

Reasonable Collection Potential (RCP): The IRS calculation of the maximum it could recover from a taxpayer based on income, assets, and allowable living expenses.

Thinking about this for your situation? Let’s talk. Contact us and we will walk you through your options – no pressure.

Offer in Compromise vs. Installment Agreement: Which Approach Works?

Where an Offer in Compromise succeeds: Settles the debt permanently for less than owed; stops penalties and interest from growing once accepted; provides a true fresh start for qualifying taxpayers.

Where an Offer in Compromise fails: Requires extensive financial disclosure; the application process runs 6 to 12 months on average; rejection leaves you back at square one with the IRS.

Where an Installment Agreement succeeds: Easier to qualify for; faster to set up (often within weeks); keeps you in good standing with the IRS while you pay.

Where an Installment Agreement fails: You pay the full debt plus ongoing interest; penalties may continue to accrue; no permanent reduction in what you owe.

| Option | Reduces Debt? | Timeline | Qualification Difficulty | Best For |

|---|---|---|---|---|

| Offer in Compromise | Yes | 6-12 months (2025) | High | Taxpayers with low RCP |

| Installment Agreement | No | 2-4 weeks | Low to moderate | Taxpayers who can pay over time |

| Currently Not Collectible | No (deferred) | Variable | Moderate | Severe short-term hardship |

The verdict: If you genuinely cannot pay the full amount and your assets plus income fall below your total tax debt, an Offer in Compromise is worth pursuing. If you have significant equity in a home, retirement accounts, or a business, an installment agreement may be the more realistic path.

Who Qualifies for an Offer in Compromise in 2025

The IRS uses a strict formula. Here is what they look at:

- Your monthly income minus your allowable monthly expenses (the IRS sets its own expense limits)

- The equity in assets you own – home equity, vehicle value, bank account balances, retirement accounts

- Whether you have filed all required tax returns

- Whether you are current on estimated tax payments (if self-employed)

- Whether you are currently in bankruptcy (you cannot apply if you are)

Recent data shows the IRS uses national and local standard expense tables to evaluate your living costs. Indiana residents in Marion County, for example, face specific IRS-allowed expense limits for housing, food, and transportation that differ from neighboring states like Illinois or Ohio. Knowing those local standards before you file your offer is critical.

According to the Taxpayer Advocate Service, many offers get rejected simply because applicants miscalculate their RCP or leave out required financial documentation.

Your Offer in Compromise Action Plan

- Step 1 – Confirm Eligibility: Use the IRS pre-qualifier tool to get a preliminary read on whether your finances suggest you qualify. This is not a guarantee, but it sets a baseline.

- Step 2 – File All Missing Returns: The IRS will reject any offer if you have unfiled tax returns. Get current before you apply.

- Step 3 – Gather Financial Documentation: Pull together three months of bank statements, pay stubs, mortgage or lease documents, vehicle loan information, and retirement account balances.

- Step 4 – Calculate Your Offer Amount: Your offer must at minimum equal your RCP. Underbidding without justification leads to rejection.

- Step 5 – Submit IRS Form 656: This is the official application. You will also complete Form 433-A (individuals) or 433-B (businesses) as a detailed financial statement.

- Step 6 – Pay the Application Fee and Initial Payment: As of 2025, the non-refundable application fee is $205. You also submit an initial payment based on your chosen payment option.

- Step 7 – Respond to IRS Requests Promptly: The IRS often asks for additional documentation. Delays on your end can result in rejection.

What to Gather Before You Apply

- ☐ Last three months of bank statements (all accounts)

- ☐ Most recent pay stubs or profit and loss statement (self-employed)

- ☐ Current mortgage or lease agreement

- ☐ Vehicle loan statements and estimated vehicle values

- ☐ Retirement and investment account statements

- ☐ Copy of all unfiled or recently filed tax returns

- ☐ Estimated tax payment records (if applicable)

- ☐ IRS notices you have received in the past 12 months

Common Mistakes That Get Offers Rejected

Firms that prepare these applications carefully typically see higher acceptance rates. The most common mistakes we see include submitting an offer amount below the RCP without proper justification, failing to include all assets in the financial statement, applying before filing all required tax returns, and underestimating how the IRS values retirement accounts. The IRS counts most retirement account balances at a discounted rate – but still counts them. Leaving that out is a red flag that triggers an automatic rejection.

Key Takeaways for Indianapolis Taxpayers in 2025

- Qualification is financial, not emotional – the IRS uses a formula, not a hardship narrative

- All returns must be filed first – no exceptions

- The application fee is $205 (2025) and is non-refundable even if rejected

- Indiana taxpayers face state-specific IRS expense standards that affect RCP calculations

- Processing runs 6 to 12 months – plan your finances accordingly

Frequently Asked Questions

How much does it cost to apply for an Offer in Compromise?

The IRS charges a $205 non-refundable application fee as of 2025. You also submit an initial payment with your application – either a lump sum deposit or the first installment of a short-term payment plan. Low-income applicants who meet IRS income thresholds may have the fee waived.

How long does the Offer in Compromise process take?

Most applications take between 6 and 12 months to process in 2025. Complex cases or incomplete submissions can extend that timeline. During review, collection activity is generally suspended, which gives you some breathing room.

What happens if the IRS rejects my offer?

You have 30 days to appeal a rejection to the IRS Office of Appeals. The appeal process can reverse the decision if you present additional documentation or correct errors in the original submission. If the appeal fails, other options like an installment agreement or Currently Not Collectible status remain available.

Can I apply for an Offer in Compromise if I am self-employed?

Yes, self-employed taxpayers in Indiana can apply, but the documentation requirements are more detailed. You will need a profit and loss statement and must be current on all estimated quarterly tax payments. Falling behind on 2025 estimated taxes while your offer is pending can cause the IRS to reject it.

Does Indiana have its own version of the Offer in Compromise?

Yes, the Indiana Department of Revenue offers a similar settlement program for state tax debt. It operates separately from the federal IRS program. If you owe both federal and Indiana state taxes, you may need to pursue both programs independently.

Will accepting an Offer in Compromise affect my credit?

The IRS does not directly report accepted offers to credit bureaus, but any existing tax liens on your record do affect your credit. Once the offer is accepted and paid, the IRS releases the lien, which can improve your credit profile over time.

What is the difference between an Offer in Compromise and Currently Not Collectible status?

Currently Not Collectible status pauses collection but does not reduce or eliminate your debt. An Offer in Compromise, once accepted and paid, permanently resolves the debt for the agreed amount. Currently Not Collectible is a temporary pause; an Offer in Compromise is a permanent resolution.

Your Next Step – Talk to Someone Who Knows This Process

The Offer in Compromise program is real, and it does help qualifying taxpayers resolve serious tax debt. But the process is detailed, the IRS scrutinizes every line of your financial submission, and a misstep early in the process can cost you months of time and your application fee.

At On-Target CPA, we work with individuals and businesses across Indianapolis, Indiana who are facing serious tax challenges. Whether you are trying to figure out if you qualify or you are ready to move forward, we can walk through the numbers with you honestly.

Ready to take the next step? Contact us today for straight answers and real solutions – because waiting only lets penalties grow.

You can also explore our services to see how we approach tax resolution and financial problem-solving for clients across Indiana.