Bookkeeping mistakes are errors in recording, categorizing, or reconciling financial transactions that cause small businesses to overpay taxes, miss deductions, and lose visibility into their actual financial position. Left unchecked, even small errors compound into serious cash flow problems and IRS exposure.

This guide focuses specifically on the bookkeeping mistakes that quietly drain small business profits, and the practical steps owners can take to stop the bleeding in 2025.

Bookkeeping Definition: Bookkeeping is the systematic process of recording daily financial transactions, reconciling accounts, and maintaining accurate financial records that support tax compliance and business decision-making.

The most common mistake we see working with small business owners is assuming their books are “close enough.” They’re not. A miscategorized expense or an unrecorded invoice can ripple into your tax return, your loan application, and your year-end cash position. According to the IRS Small Business and Self-Employed Tax Center, inadequate recordkeeping is one of the leading triggers for audits and penalties among small businesses.

The Bookkeeping Mistakes Most Small Business Owners Don’t See Coming

These aren’t dramatic errors. They’re the quiet ones that stack up month after month.

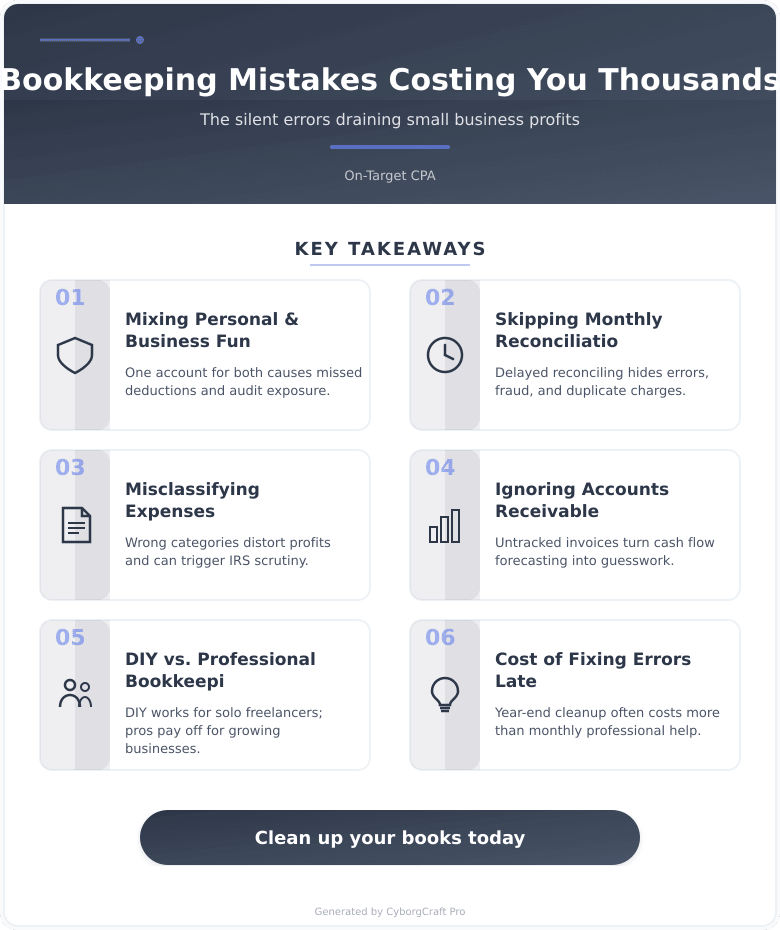

Mixing personal and business finances: Using one bank account for both personal and business spending creates a recordkeeping nightmare. Deductions get missed. Expenses get misclassified. And if you’re ever audited, you’ll spend hours untangling transactions that should never have been combined.

Falling behind on reconciliation: Reconciling your accounts monthly catches errors, duplicate charges, and fraud early. Businesses that skip this step often discover problems only at tax time, when fixing them is expensive and stressful.

Misclassifying expenses: Putting a marketing expense under “office supplies” or a contractor payment under “payroll” doesn’t just look messy. It distorts your profit reports, misstates your taxable income, and can trigger questions from the IRS.

Ignoring accounts receivable: If you’re not tracking what clients owe you, cash flow projections become guesswork. Consistent AR tracking helps businesses stay on top of outstanding invoices and supports stronger collection outcomes over time.

Want to explore this further? Our services page outlines how On-Target CPA helps Indianapolis-area businesses build clean, reliable books from the ground up.

DIY Bookkeeping vs. Professional Bookkeeping: Which Approach Works?

Where DIY bookkeeping succeeds: Lower upfront cost, full control over timing, works reasonably well for sole proprietors with minimal transactions.

Where DIY bookkeeping fails: Owners lack time to stay current, tax law changes go unnoticed, errors accumulate undetected, and year-end cleanup costs often exceed what professional help would have cost monthly.

Where professional bookkeeping succeeds: Consistent monthly close, accurate categorization, tax-ready financials, and a second set of eyes on cash flow trends. Businesses using professional bookkeeping services report fewer year-end surprises and stronger audit readiness.

Where professional bookkeeping fails: Higher monthly cost for very simple businesses, requires owner involvement to share receipts and context promptly.

The verdict: For most small businesses with multiple revenue streams, employees, or contractor relationships, professional bookkeeping pays for itself by preventing errors that cost more to fix. DIY works best only for the simplest, lowest-volume operations.

| Approach | Monthly Cost Range | Best For | Risk Level |

|---|---|---|---|

| DIY Software Only | $20 – $80 | Solo freelancers, minimal transactions | High without training |

| Bookkeeping Service | Varies by provider and scope | Small businesses, growing teams | Low with good provider |

| Full-Service CPA Firm | Varies by complexity and services | Complex entities, tax strategy needs | Lowest |

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options, no pressure.

Your Bookkeeping Action Plan

- Step 1 – Separate accounts immediately: Open a dedicated business checking account and business credit card this week. This single step eliminates the most common source of bookkeeping errors.

- Step 2 – Set a monthly reconciliation date: Block 90 minutes on the last Friday of every month to reconcile your bank and credit card statements. Consistency matters more than perfection.

- Step 3 – Build a chart of accounts: Work with a CPA or bookkeeper to create expense categories that match your business model and Indiana tax requirements. Under current Indiana law (2025), accurate expense categorization directly affects your state adjusted gross income calculation.

- Step 4 – Track receivables weekly: Use your accounting software’s AR aging report every Friday. Any invoice over 30 days should trigger a follow-up.

- Step 5 – Review financials monthly, not just at tax time: A monthly profit and loss review takes 20 minutes and catches problems before they become costly.

Indiana-Specific Bookkeeping Considerations in 2025

Indiana’s flat individual income tax rate was approximately 3.05%-3.15% around 2025, subject to annual legislative adjustments. For pass-through entities like S-corps and sole proprietors based in Indianapolis, accurate income tracking directly affects your Indiana state tax liability. The Indiana Department of Revenue also requires businesses with employees to maintain payroll records for at least three years, a compliance detail many small business owners overlook.

Compared to neighboring states, Indiana’s compliance requirements are relatively straightforward. Ohio requires commercial activity tax filings for businesses above a gross receipts threshold. Illinois carries significantly higher income tax rates for pass-through income. Proper bookkeeping helps Indiana businesses take full advantage of their relatively favorable tax position.

What to Gather Before Your First Bookkeeping Review

- ☐ Last 12 months of bank statements (all business accounts)

- ☐ Credit card statements for all cards used for business

- ☐ Prior year business tax return

- ☐ Outstanding invoices and bills

- ☐ Payroll records if you have employees or contractors

- ☐ Receipts for any major asset purchases

Key Takeaways for Small Business Owners in 2025

- Mixing personal and business finances is the single most disruptive bookkeeping mistake, creating tax risk and wasted time.

- Monthly reconciliation is non-negotiable for catching errors before they compound.

- Expense misclassification distorts profits and can overstate or understate your taxable income.

- Indiana’s 2025 tax rate makes accurate income tracking more valuable than ever for pass-through entity owners.

- Professional bookkeeping typically costs less than the mistakes it prevents, especially for growing businesses.

Frequently Asked Questions

What are the most common bookkeeping mistakes small businesses make?

The most common bookkeeping mistakes include mixing personal and business finances, skipping monthly reconciliation, and misclassifying expenses. These errors distort your financials, increase tax liability, and create audit risk. Most are preventable with simple systems and consistent habits.

How much does professional bookkeeping cost for a small business in 2025?

Professional bookkeeping costs vary depending on transaction volume, business complexity, and the scope of services provided. Full-service CPA firms handling both bookkeeping and tax strategy may run higher. Most owners find the cost is offset by tax savings and avoided correction fees.

How often should I reconcile my business bank accounts?

Monthly reconciliation is the standard best practice for small business bookkeeping. Waiting longer than 30 days makes it harder to catch errors, spot fraud, or identify duplicate charges before they create cascading problems in your financial reports.

Can bookkeeping mistakes trigger an IRS audit?

Yes, poor recordkeeping and inconsistent financial reporting are recognized audit risk factors according to IRS guidance. Mismatched income figures, large unexplained deductions, and missing 1099 documentation are common triggers. Clean, consistent books significantly reduce your audit exposure.

What is the difference between bookkeeping and accounting?

Bookkeeping is the daily recording of transactions; accounting uses that data for analysis, tax preparation, and financial planning. Bookkeeping feeds accounting. Without accurate books, your CPA’s tax strategy and financial advice are built on shaky ground.

How do Indiana’s bookkeeping requirements differ from neighboring states?

Indiana requires businesses to retain payroll and financial records for at least three years, consistent with IRS guidelines, and the state’s relatively straightforward flat income tax structure simplifies some calculations compared to Ohio or Illinois. Pass-through entity owners in Indiana benefit from accurate income tracking given the state’s ongoing rate adjustment schedule.

Your Next Step

Bookkeeping errors don’t announce themselves. They hide in miscategorized expenses, unreconciled accounts, and ignored receivables until they show up as a surprise tax bill or a cash flow crisis. The good news is that most of these problems are fixable quickly with the right help.

At On-Target CPA, serving small businesses in Indianapolis, Indiana, we work with owners who are ready to get their numbers right and keep them that way. Ready to take the next step? Contact us today for straight answers and real solutions. The sooner your books are clean, the sooner you can make decisions with confidence.