You Got an IRS Letter – Now What? A Step-by-Step Guide for Indianapolis Business Owners

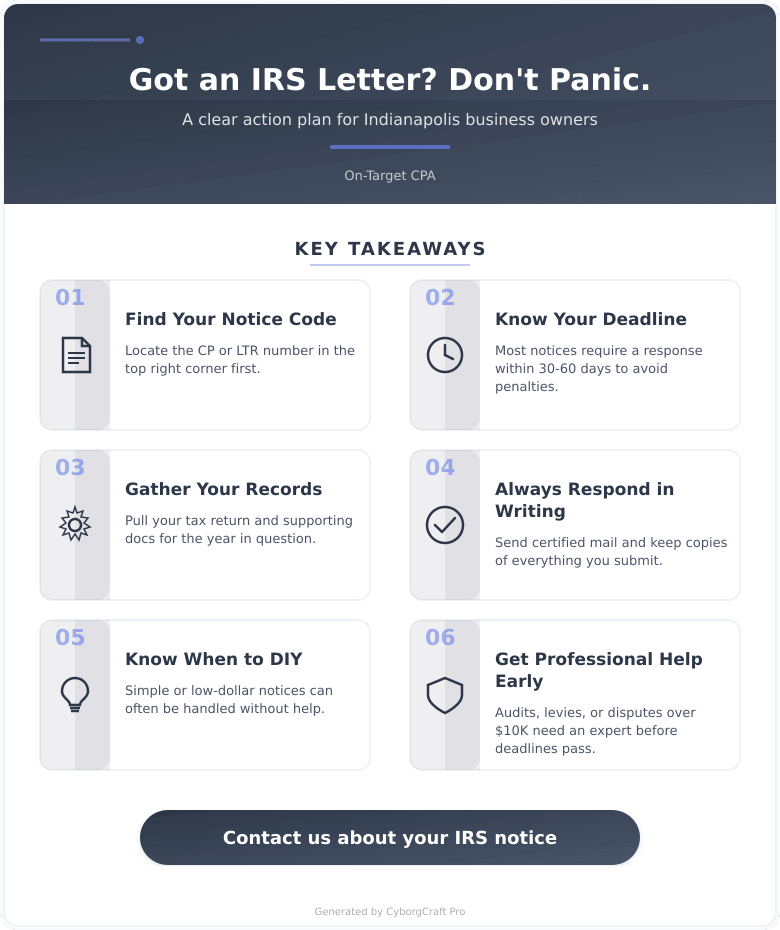

Getting an IRS letter as a business owner triggers immediate stress – but most notices are manageable when you know how to read them and respond correctly. Every IRS notice carries a CP or LTR code in the upper right corner that tells you exactly what the agency wants, whether that is a missing return, a balance due, a discrepancy in reported income, or a more urgent collection warning. The biggest mistake business owners make is ignoring the notice and hoping it goes away – it never does, and the consequences compound quickly. This post walks through a clear six-step response process: identify the notice code, note the deadline, gather supporting tax records, determine whether you agree or disagree with the IRS finding, respond in writing via certified mail, and track your case until resolved. A comparison of notice types – from simple CP14 balance due notices to serious LT11 levy warnings – helps readers quickly gauge the urgency of their situation. The post also covers when handling a notice independently makes sense versus when bringing in a CPA is the smarter move, particularly for CP2000 underreporter notices, audits, or multi-year issues. Indianapolis business owners will find specific guidance on common mistakes, required documents to gather before responding, and what 2025 IRS enforcement activity means for response timelines. On-Target CPA, located in Indianapolis, Indiana, helps business owners navigate IRS correspondence with a structured, documented approach that protects their interests from the first response forward.

The Most Important Succession Planning Change for Main Street Business Owners in Years

By Michael Jamison, CPA, CGMA For years, I have had the same frustrating conversation with successful business owners. They spent decades building a company. They created jobs. They developed leaders. They built a culture that mattered. When the time came to think about succession, their first choice was often clear: sell the business to […]

Offer in Compromise: The IRS Program That Can Settle Your Tax Debt for Less Than You Owe

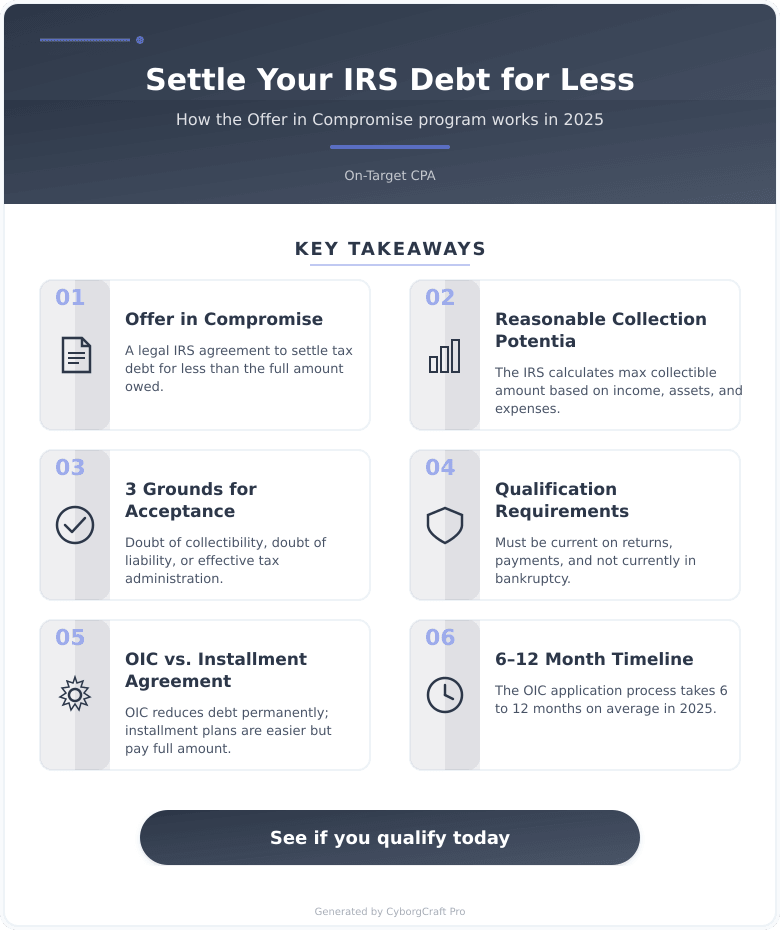

An Offer in Compromise is one of the few IRS programs that actually allows taxpayers to settle federal tax debt for less than the full amount owed. The key is understanding that the IRS accepts these offers based on a precise financial formula – your Reasonable Collection Potential – not simply because you are struggling. This post breaks down exactly how the program works in 2025, the three grounds for acceptance, and how an Offer in Compromise compares to alternatives like installment agreements and Currently Not Collectible status. Indiana taxpayers face state-specific IRS expense standards that affect how the agency calculates what you can pay, and those local numbers matter. The post walks through a complete seven-step action plan, a document checklist for applicants, and the most common mistakes that lead to rejection. A dedicated FAQ section covers costs (the 2025 application fee is $205), timelines (6 to 12 months), the appeal process, self-employment complications, and how Indiana’s own state tax settlement program operates separately from the federal one. The content is designed to help readers quickly assess whether they might qualify and what concrete steps to take next.

The Bookkeeping Mistakes That Cost Small Businesses Thousands Every Year (And How to Stop Making Them)

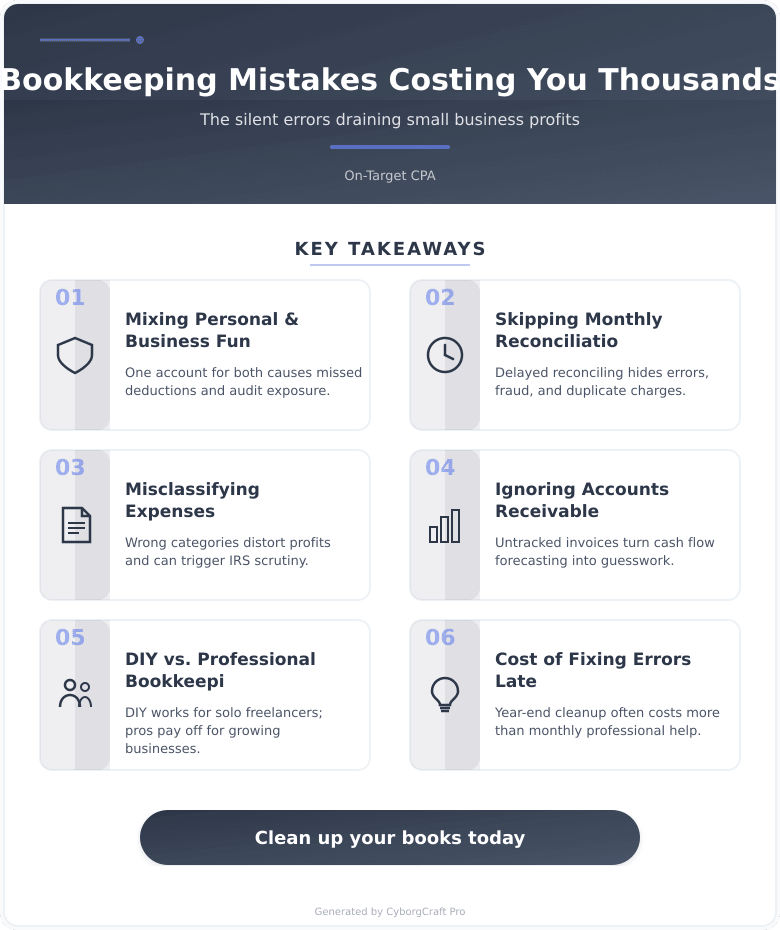

Small business bookkeeping mistakes are far more expensive than most owners realize, and they rarely announce themselves until tax season or a cash flow crisis. The most damaging errors include mixing personal and business finances, skipping monthly bank reconciliation, misclassifying expenses, and ignoring accounts receivable. Each of these problems distorts financial reports, inflates tax liability, and creates IRS audit exposure. For Indianapolis-area businesses in 2025, Indiana’s updated flat income tax rate makes accurate income tracking especially valuable for pass-through entity owners. The post compares DIY bookkeeping against professional services with a cost table showing 2025 market rates, and delivers a five-step action plan covering account separation, monthly reconciliation, proper chart-of-accounts setup, AR tracking, and monthly financial reviews. A preparation checklist outlines exactly what business owners should gather before their first bookkeeping review. The FAQ section covers audit risk, reconciliation frequency, cost benchmarks, and the difference between bookkeeping and accounting. The core message is clear: professional bookkeeping typically costs less than the mistakes it prevents, and clean books are the foundation of every smart financial decision a business owner makes.

Buying a Business in Indianapolis? Here’s What Your CPA Needs to Review Before You Sign Anything

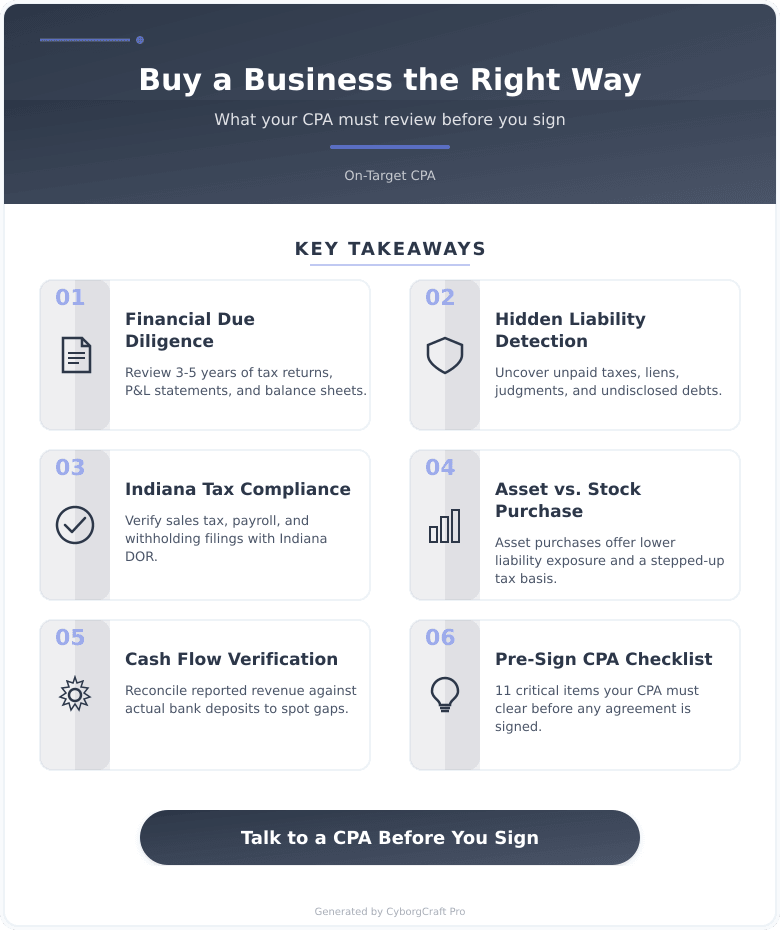

Buying a business without a proper CPA review is one of the most common and costly mistakes Indianapolis buyers make. This post breaks down exactly what a pre-acquisition financial review should cover, from reconciling tax returns and P&L statements to obtaining Indiana Department of Revenue tax clearance certificates that protect buyers from successor liability. The asset purchase vs. stock purchase comparison shows why deal structure matters for long-term tax exposure, with a clear recommendation for most small business deals. Indiana-specific issues get direct attention, including the state’s pass-through entity tax election changes in 2025 and how neighboring states like Ohio, Illinois, Michigan, and Kentucky compare on clearance processes and risk. A full step-by-step action plan gives buyers a practical roadmap, and the six-question FAQ section covers costs, timelines, liability rules, and earnings recasting in plain terms. The post positions the CPA as a critical pre-signing partner rather than an afterthought, with two soft CTAs and a strong closing call-to-action directing readers to On-Target CPA in Indianapolis.

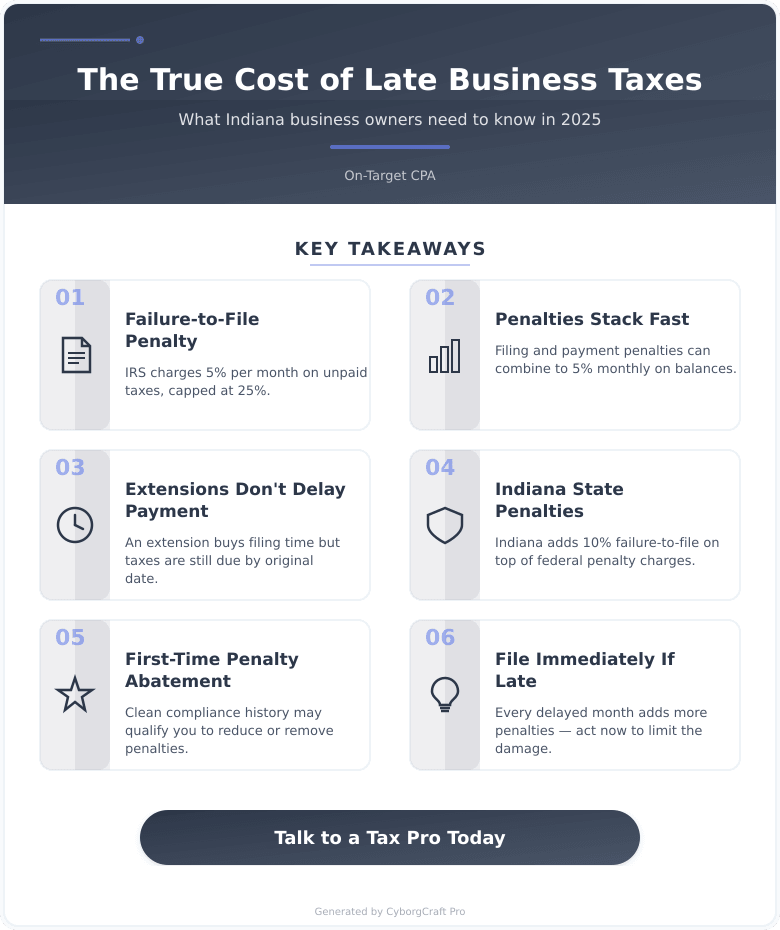

The Real Cost of Filing Your Business Taxes Late – And What You Can Actually Do About It

Filing a business tax return late in Indiana can cost far more than most owners realize. The IRS charges a 5% per month failure-to-file penalty on unpaid taxes, capped at 25%, plus a separate 0.5% per month failure-to-pay penalty. Indiana adds a 10% state penalty on top of unpaid state balances, and for pass-through entities like LLCs and S-Corps, those penalties can flow to individual owners as well. The post breaks down exactly how these charges stack, clarifies the critical difference between filing an extension and actually deferring payment, and explains two paths to penalty relief: First-Time Penalty Abatement for businesses with a clean three-year compliance record, and reasonable cause abatement for those who experienced genuine documented hardship. A comparison of the extension-vs-late-filing tradeoffs shows that while extensions protect against failure-to-file penalties, they do not stop payment-related penalties from running. A five-step action plan walks business owners through filing immediately, making partial payments, reviewing compliance history, documenting hardship, and formally requesting relief. The post also includes a preparation checklist so readers know exactly what to gather before consulting a CPA, plus a full FAQ section addressing common questions about timelines, Indiana-specific rules, and how long resolution typically takes. On-Target CPA serves business owners in Indianapolis, IN and surrounding communities.

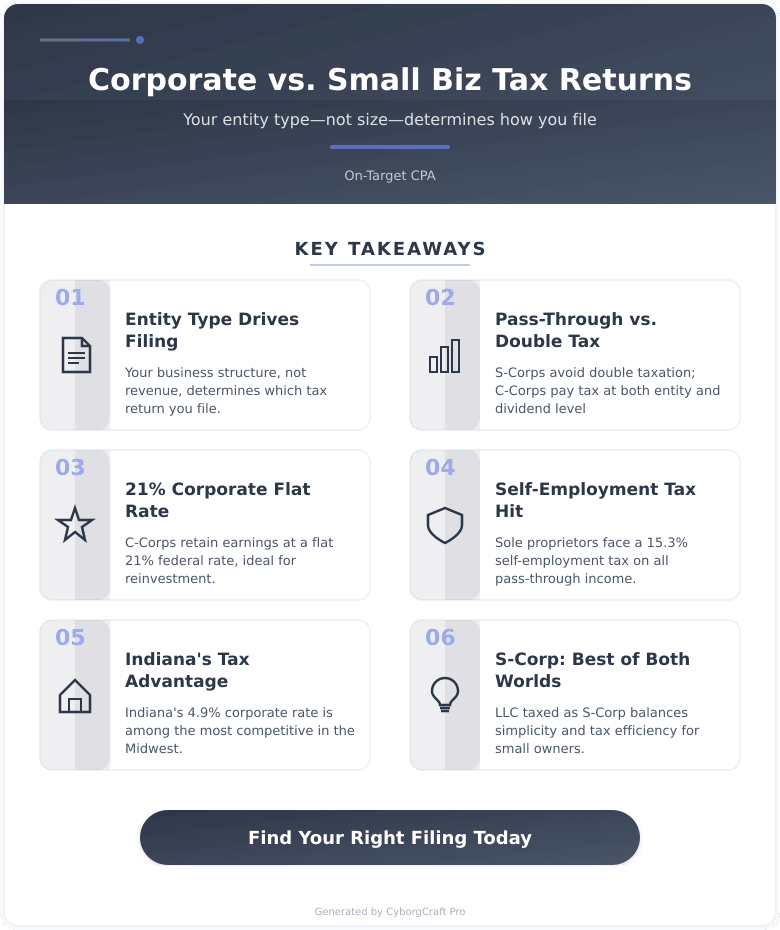

Corporate Tax Return vs. Small Business Tax Return: What’s the Difference and Which One Do You Need?

Choosing the wrong tax return type is one of the most common and costly mistakes Indiana business owners make. Your entity structure – not your revenue or headcount – determines whether you file a corporate return like Form 1120 or a pass-through return like Schedule C or Form 1065. C-Corps pay tax at the entity level at a flat 21% federal rate, but face double taxation on dividends. S-Corps and sole proprietors use pass-through treatment, meaning income flows to the owner’s personal return. Indiana’s 4.9% corporate tax rate is competitive compared to Illinois, Michigan, Ohio, and Kentucky, but still requires a separate state filing. LLCs are especially confusing because their tax treatment depends entirely on IRS elections made at formation or later. Key 2025 deadlines include March 17 for S-Corps and partnerships, and April 15 for C-Corps and sole proprietors. Filing the wrong form can trigger audits, missed deductions, and penalties. The post walks through a practical action plan, a document checklist, and a clear comparison of each entity type, form, and estimated preparation cost – giving Indianapolis business owners the clarity they need before tax season gets away from them.

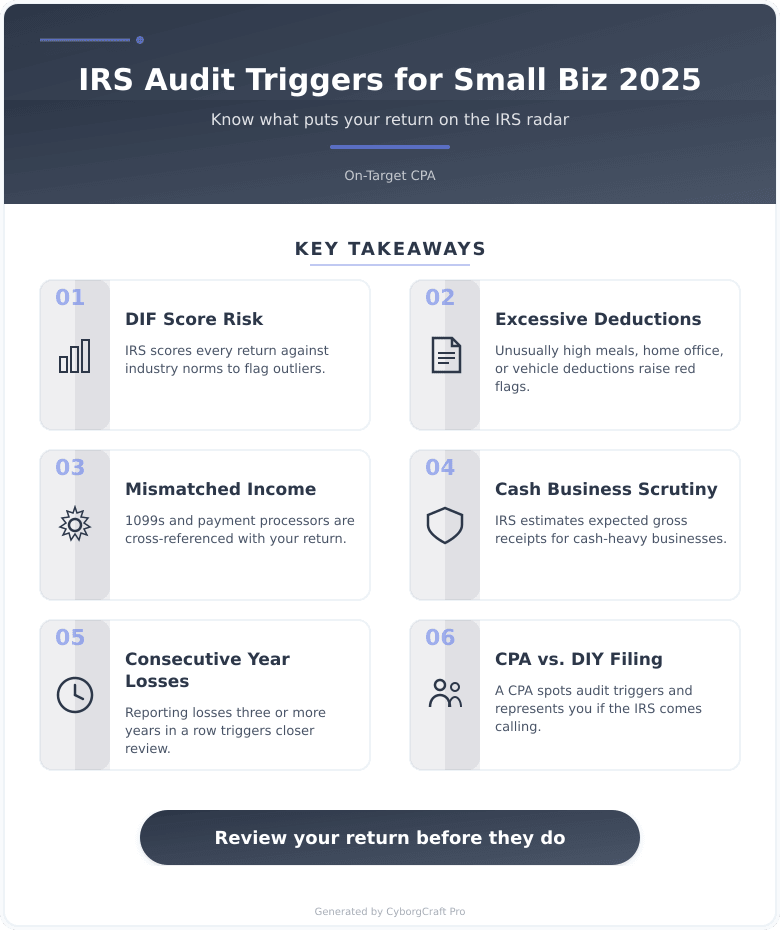

IRS Audit Triggers for Small Businesses in 2026: What’s on Their Radar Right Now

Small business owners in 2025 face a more active IRS than in recent years, thanks to upgraded data matching tools and increased enforcement funding. This post breaks down the specific audit triggers that are drawing the most IRS attention right now, including income mismatches with third-party 1099s, disproportionate deductions, cash-based business reporting gaps, and consecutive years of reported losses. It explains how the IRS’s automated Discriminant Income Function scoring system works and what pushes a return into review territory. A clear comparison of DIY filing versus working with a CPA shows why professional review offers meaningful protection for businesses with multiple deductions or employees. A practical five-step action plan and pre-filing checklist give business owners concrete steps to take before submitting their returns. Indiana-specific risks are addressed, including the likelihood of parallel state review when the IRS flags a return. The post closes with a direct call to action for Indianapolis-area business owners to connect with On-Target CPA for a proactive return review before any problems arise.

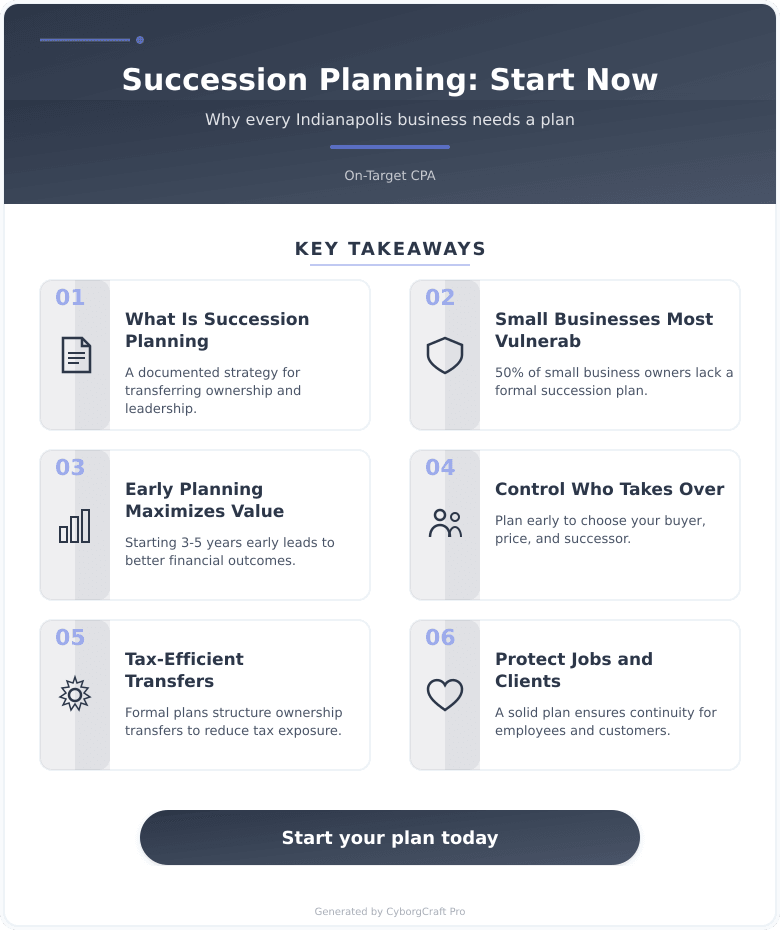

Succession Planning Is Not Just for Big Companies – Why Every Indianapolis Business Owner Needs a Plan Now

Succession planning is one of the most overlooked financial priorities for small and mid-size business owners. Most owners assume it is something only large corporations worry about, but the opposite is true – smaller businesses are often more vulnerable when leadership or ownership suddenly changes with no plan in place. This post breaks down why Indianapolis business owners should treat succession planning as a present-day priority rather than a future concern. It covers the core definition of succession planning, why starting 3-5 years before exit leads to better financial outcomes, and how deal structure affects tax exposure under both Indiana and federal law in 2025. A clear comparison between informal and formal planning approaches shows the real cost of doing nothing. A step-by-step action plan walks owners through valuation, identifying successors, tax structuring, business documentation, buy-sell agreements, and annual reviews. A document checklist helps owners prepare for a first planning conversation. Key takeaways are organized for fast reference, and a detailed FAQ section answers the most common questions – including what happens in Indiana probate without a plan, how employee buyouts work, and how succession planning differs from estate planning. The post connects readers to On-Target CPA in Indianapolis for straightforward, no-pressure guidance on their specific situation.

ABCs of customer profitability

Some customers naturally require more time and resources than others. But when certain relationships consistently consume more of your and your employees’ time than they generate in profit, it may be time to reassess. Taking a closer look at customer‑level profitability can help you understand where resources are going and ensure that high‑value relationships receive […]