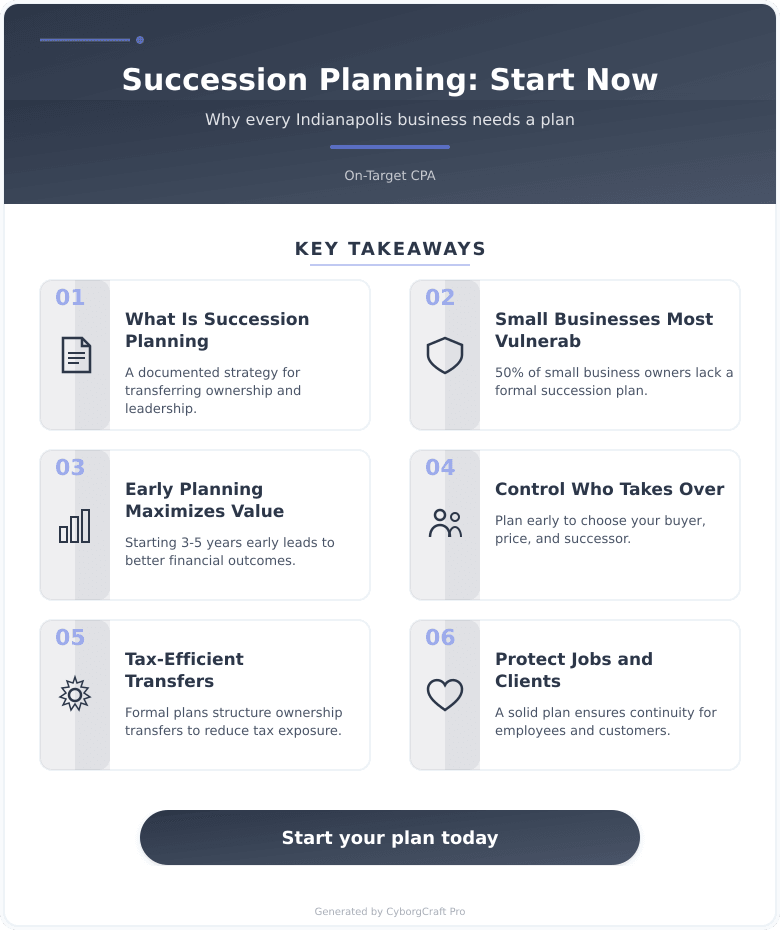

Business succession planning is the process of preparing for the transfer of ownership, leadership, or both when a business owner retires, exits, or passes away. A well-built succession plan protects the business’s value, preserves jobs, and ensures continuity for clients and employees alike.

This guide focuses specifically on why Indianapolis small and mid-size business owners need a succession plan in 2025, and what actionable steps to take right now.

Succession Planning Definition: A succession plan is a documented strategy outlining how business ownership and leadership will transfer to a new owner, family member, key employee, or outside buyer when the current owner steps away.

Most business owners in Indianapolis assume succession planning is reserved for large corporations with boards and legal departments. The reality is different. Small businesses are often more vulnerable to sudden ownership gaps because there is no safety net of redundant leadership. One unexpected health event, one divorce, one retirement with no plan in place – and the business can collapse in weeks.

According to the U.S. Small Business Administration, small businesses account for 99.9% of all U.S. firms, yet studies show around 50% or fewer of small business owners have a formal succession plan, varying by source. That gap is where businesses quietly lose their value.

Why Business Succession Planning Matters More Than You Think

Here is the thing – most owners do not think about succession until something forces them to. A health scare. A partner who wants out. A potential buyer calling out of the blue. By then, the business is often in reactive mode, and reactive decisions rarely produce the best outcomes.

Business succession planning done early lets you control the narrative. You choose the buyer. You set the price. You decide whether family takes over or a key employee does. You protect your employees’ jobs and your clients’ relationships. Without a plan, those decisions get made by circumstance.

The most common mistake we see is owners waiting until they are emotionally ready to retire before addressing succession. By that point, there is rarely enough runway to groom a successor, structure the deal tax-efficiently, or maximize the sale price. Businesses that start planning 3-5 years before an exit typically achieve meaningfully better financial outcomes than those that wait.

Thinking about this for your situation? Let’s talk. We’ll walk you through your options – no pressure. Contact us to get a conversation started.

Planning With No Plan vs. Planning With a Strategy: Which Approach Works?

Where informal (no plan) approaches succeed: They require zero upfront effort, and for very small one-person operations with no employees and minimal assets, there may be little to transfer anyway.

Where informal approaches fail: They leave the business’s value unprotected. They create tax exposure at transfer. They put employees and clients at risk of disruption. They often result in undervalued sales because the owner has no leverage when urgency forces a quick decision.

Where formal succession planning succeeds: It maximizes sale price through early valuation work. It structures ownership transfer in a tax-efficient way under Indiana law. It documents processes and leadership so the business can run without the original owner.

Where formal succession planning can feel difficult: It requires honest conversations with family members, co-owners, and key employees. It takes time. And yes, it means facing the reality that you won’t run this business forever.

The verdict: For any Indianapolis business with employees, clients, intellectual property, or real revenue, a formal succession plan is not optional if you want to protect what you built. The short-term effort pays back far more than it costs.

| Approach | Avg. Timeline | Tax Efficiency | Best For |

|---|---|---|---|

| No formal plan | Reactive (weeks) | Low | Solo freelancers with minimal assets |

| Key employee buyout | 2-5 years | Moderate-High | Businesses with strong internal leadership |

| Family transfer | 3-7 years | High with planning | Family businesses with willing successors |

| Third-party sale | 1-3 years prep | High with planning | Owners seeking maximum sale value |

See how our approach compares – visit our services page to learn what financial planning support looks like for Indianapolis business owners.

Your Succession Planning Action Plan

- Step 1 – Get a Business Valuation: You cannot plan an exit without knowing what the business is actually worth. A professional valuation sets the baseline and reveals gaps that reduce value.

- Step 2 – Identify Your Successor Options: Family member, key employee, outside buyer, or merger. Each path has different tax treatment under Indiana law and federal IRS rules in 2025.

- Step 3 – Address the Tax Implications Early: A transfer structured correctly can dramatically reduce capital gains exposure. Waiting until the deal is done leaves money on the table.

- Step 4 – Document Business Operations: A business that depends entirely on the owner’s knowledge does not transfer cleanly. Documented systems increase value and buyer confidence.

- Step 5 – Draft or Update Your Buy-Sell Agreement: If you have a business partner, this is non-negotiable. Partnership disputes that arise from the absence of a clear buy-sell agreement can be costly and disruptive, making this document an essential safeguard.

- Step 6 – Review and Revise Annually: Tax law changes. Business value changes. Indiana regulatory requirements evolve. Your succession plan should be reviewed every 12 months.

What to Gather Before Your First Succession Planning Meeting

- ☐ Most recent 3 years of business tax returns

- ☐ Current profit and loss statements and balance sheets

- ☐ Existing buy-sell agreements or partnership agreements

- ☐ List of key employees and their tenure

- ☐ Any existing business valuation documents

- ☐ Personal financial goals and retirement timeline

- ☐ Life insurance policies tied to the business

Key Takeaways for Indianapolis Business Owners in 2025

- Start early – Owners who begin business succession planning 3-5 years before exit consistently get better financial outcomes.

- Know your value – A current business valuation is the foundation of any solid plan.

- Tax structure matters – How you transfer ownership has real dollar implications under both Indiana and federal tax law in 2025.

- Document everything – A business that runs without you is worth significantly more than one that does not.

- Review annually – Laws and business conditions change; your plan should keep up.

Frequently Asked Questions

What is business succession planning and why does it matter for small businesses?

Business succession planning is the process of preparing for the transfer of ownership or leadership before it becomes urgent. For small businesses in Indianapolis, it protects employees, clients, and the financial value the owner has built over years of work.

When should an Indianapolis business owner start succession planning?

The right time to start is at least 3-5 years before you plan to exit or retire. Starting early gives you time to build value, structure the transfer tax-efficiently, and avoid making rushed decisions under pressure.

What does succession planning typically cost in 2025?

Costs vary based on business complexity, but general industry ranges for succession planning support run from a few thousand dollars for basic documentation to significantly more for complex multi-owner businesses. The cost is almost always far less than the financial loss from an unplanned or poorly structured exit.

Does Indiana have specific tax considerations for business transfers?

Yes – Indiana does not have a state inheritance tax, but federal capital gains and estate tax rules still apply to business transfers in 2025. How the deal is structured, whether as an asset sale or stock sale, has real tax consequences that vary under current IRS guidelines. According to the Internal Revenue Service, deal structure is one of the most significant factors affecting after-tax proceeds from a business sale.

What happens if a business owner dies without a succession plan in Indiana?

Without a plan, the business typically goes through probate, which can freeze operations, create disputes among heirs, and result in a forced sale at below-market value. Indiana probate timelines can stretch months or longer, during which the business may lose clients, employees, and revenue.

Can a key employee buy out the business instead of selling to an outside buyer?

Yes, an employee buyout is a common and often tax-advantaged succession path for Indiana business owners. Structures like seller-financed deals or Employee Stock Ownership Plans (ESOPs) can make it work financially for both sides, but they require careful planning well in advance.

How does succession planning differ from estate planning?

Estate planning addresses what happens to your personal assets after death, while business succession planning specifically addresses the continuity and transfer of the business itself. The two overlap significantly and should be coordinated together, especially for business owners whose company is their largest personal asset.

Your Next Step Starts Here

There is no perfect moment to start succession planning – but there is a cost to waiting. Every year without a plan is a year of risk, and 2025 is a good time to change that. Whether you are 5 years from retirement or 15, getting clarity on your options now means more control and better outcomes when the time comes.

At On-Target CPA, we work with business owners in Indianapolis, Indiana to think through these decisions clearly – from valuation to tax strategy to the structure of the transfer itself. Our office is located at 101 West Ohio Street, Suite 800, Indianapolis, IN 46204, and we work with owners across the Indianapolis area.

Ready to take the next step? Contact us today for straight answers and real solutions – no jargon, no pressure, just a clear conversation about where you stand and what your options are.